If you've been following the creative financing series Peter Baldwin and I have been putting together, you know the core premise by now: the capital stack is the risk management document. Every instrument in it is an answer to a specific question about who holds which risk, in what form, and for how long.

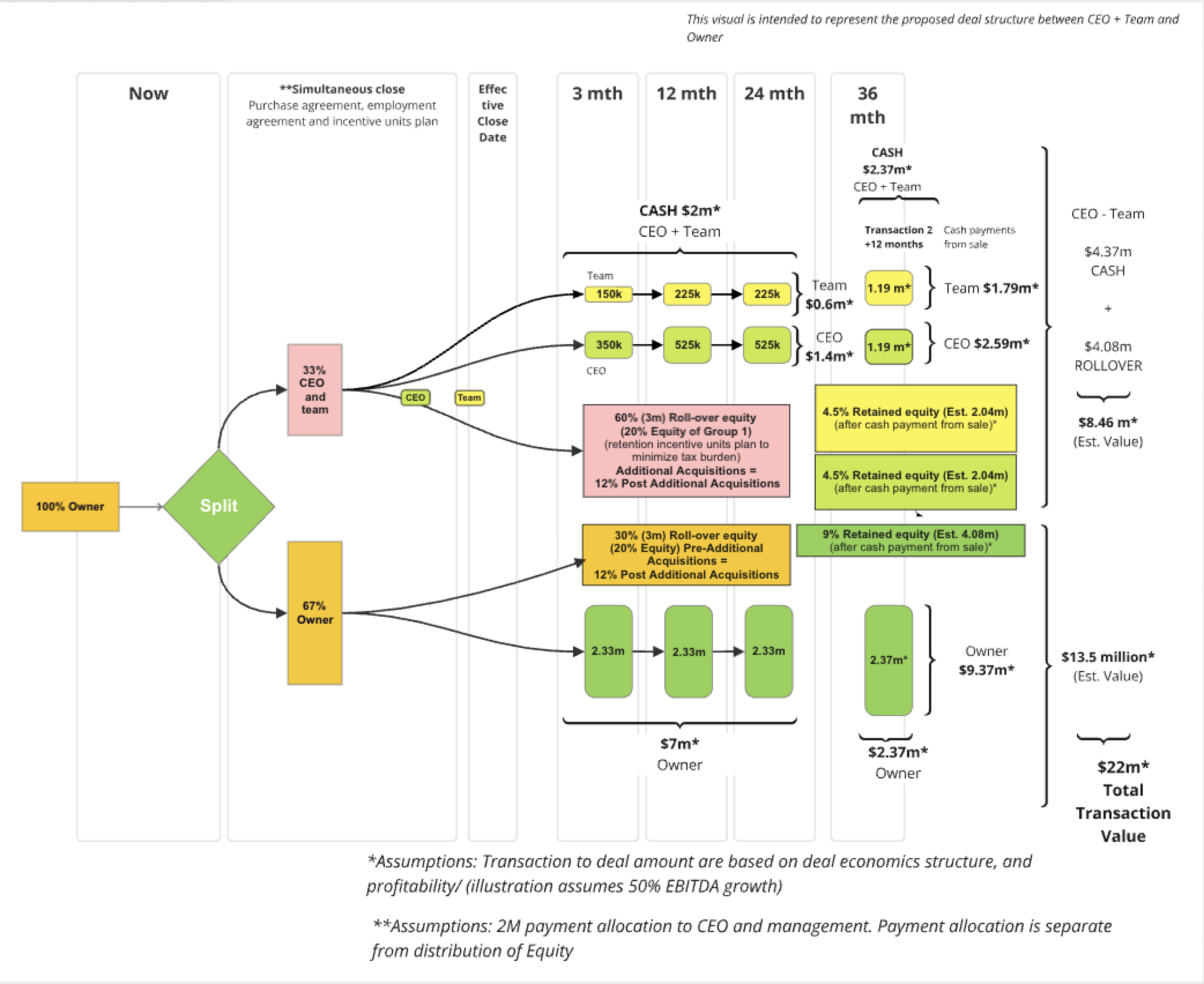

This episode is different from the others. Instead of walking through a framework, we walked through an actual deal: numbers, motivations, stakeholders, and all the structural decisions we made along the way. We built an illustration of this transaction to share with the parties involved, and we're walking through that same visual here.

The Business: What We Were Looking At

The company had roughly $3 million in annual profit. The owner was not involved in day-to-day operations. He was, in Peter Baldwin's words, simply harvesting the cash at that point. The entire operational weight of the business sat on a senior management team: a CEO and a small executive team, none of whom had any equity stake. They were all salaried employees.

The business also had some real watch-outs.

High customer concentration: one client represented more than half of total revenue. That client had a contract renewal coming up shortly after we intended to close. And the owner, the person we were negotiating with, wasn't the person keeping the lights on. The team was.

None of that made the deal undoable. All of it shaped how we had to structure it.

Three Constituencies, Three Different Problems

Before we get into the structure, it's worth being clear about who we were actually solving for. Most deal conversations treat this as a bilateral negotiation: buyer and seller. This one had three distinct groups whose interests we had to design around.

The owner wanted to exit. He had a reason to transact on a specific timeline, which gave us some urgency to work with but also meant we couldn't afford to lose the deal over disagreement on structure.

The CEO was the real operational fulcrum. No long-term contract. No equity stake. Nothing formally tying him to the business post-close. If the CEO walked, the business had a serious problem and so would any future buyer.

The senior management team had the same problem at a smaller scale. They were the reason the key client stayed, the reason the work got done, and the reason the business was generating $3 million in profit for an absent owner. They had no stake in any of it.

We went to the seller with a direct message: you need to help us bind your team and share some of the upside with them in order to create an asset that's worth selling. Because without them, there's no long-term value here.

He heard us.

The Headline Number and How We Got There

We valued the business at five times profit: $15 million in total value. But the headline purchase price and the total deal value are two different things, and it's important to understand the distinction.

The seller received $10 million in consideration: $3 million in rollover equity (a 20% non-voting Class B stake in the combined entity) and a $7 million seller note structured across three tranches. The rollover equity wasn't cash, it was treated as a reinvestment into the go-forward business.

The remaining $5 million in value was allocated to the employee group: $2 million in cash retention bonuses and $3 million in profits interest units (PIUs) in the new entity. That consideration wasn't part of the formal purchase price. Accounting-wise, it runs through as ordinary compensation. But from a total value perspective, it was very much part of what we were putting on the table.

So: $10 million purchase price, $15 million in total deal value, for a business doing $3 million in profit. The effective purchase price multiple was around 3.3x. The total value multiple was 5x. The gap between those two numbers is exactly where the structure lives.

Tying Payments to Risk, Not Just Time

The seller note didn't amortize on a straight calendar schedule. The tranches were tied to events: specifically, the events we identified as the biggest risks in the transaction.

The first tranche was structured around the contract renewal. The largest client, the one representing more than 50% of revenue, had a renewal coming. We weren't going to wait to close until after it came in, the seller had a timeline and we had to move, but we could tie consideration to the outcome. The initial tranche of the seller note was set to hit on the later of a fixed date or the contract renewal event.

It ended up coming in about four and a half months after close. We had structured for six months just in case.

This is the principle Peter and I come back to across almost every deal: payment timing should reflect the distribution of risk. You can structure installments by time or by trigger. When the biggest risk in a business is a specific, identifiable event, you use that event as the trigger. It aligns interests and it gives the seller a clear path to accelerating payment if the business performs.

What We Did with the Employee Pool

The $5 million employee package was split into two buckets: $2 million in cash retention bonuses and $3 million in PIUs.

We gave the CEO full discretion over how to allocate within that pool. He knew his team better than we did. He knew who was indispensable, who was a flight risk, who was likely to be duplicative if we brought in a strategic buyer down the line, and who he needed to protect.

We did share some principles with him about how we thought about the structure:

For people whose roles were likely to be duplicative at exit — where a strategic acquirer probably wouldn't need that function — we back-ended the compensation. The majority of their retention bonus sat at the 24-month mark, not at close.

For people who were flight risks but critical to client retention, we loaded more comp toward the earlier payments. We needed them around for at least the first year. The structure reflected that.

For the CEO himself, the split was roughly 25% upfront, with the remaining 75% tied to the same installment sequence as the seller note.

We ended up paying out about 75-80% of the retention pool in total — a mix of some regrettable voluntary attrition and some involuntary that was entirely appropriate. The core team made it to exit.

The PIUs and the Pre-Negotiated Roll

The profits interest units weren't standard equity. They came with a threshold: the Class A investors and the Class B member (the original seller, who rolled in) had to have their capital accounts drained to zero before the management team could participate in any upside.

More importantly, we pre-negotiated what happened to those PIUs at exit.

This is the part most buyers skip. They think about binding management through the first transaction. They don't think about what happens when they go to sell. We did.

Only a portion of the PIUs vested on our exit. The remainder was forcibly rolled — at buyer discretion — into the successor entity. Management then had to hold for an additional 12 months before they could cash out that second tranche.

When we went to market to sell the business, we weren't just selling a well-run agency. We were selling a management team that was contractually and economically bound to stick around for the buyer. The team had already demonstrated they believed in the business enough to defer consideration. And they had skin in the game at the new entity before the transaction even closed.

That's not a small thing when you're trying to command a premium on exit.

Knowing the Buyer Before You Buy

Peter mentioned something that I want to make sure doesn't get buried: we knew who the buyer was going to be before we closed the entry transaction.

That's not always possible. But when it is, it changes everything about how you design the deal. You're not building toward a generic exit. You're building toward a specific conversation with a specific counterparty who you've already had preliminary discussions with.

In this case, we had talked to the likely strategic buyer before we transacted. They told us they'd follow the journey, stay in the loop, and we kept them informed as we built the business out. When it came time to exit, we weren't selling a business cold to an unknown buyer. We were delivering on a thesis we'd communicated years earlier.

The practical implication for how we structured the deal: we knew what that buyer would care about. We knew what would move the valuation on their side. And we designed the team incentive structure and the management rollover specifically to make the asset as easy as possible for them to absorb.

Beginning with the end in mind isn't a philosophical preference. It's a structural discipline. If you know who the buyer is, you can build the business they want to buy.

The Model Behind the Visual

The illustration we shared with the parties is the visible part of the iceberg. Below the waterline is a financial model: monthly cash flows for at least the first 12 months, quarterly from there out, with the full sequence of seller note payments, retention comp outflows, and equity distributions mapped across the full hold period.

This business happened to be negative working capital, which helped. The largest client paid inside the payroll cycle, and vendor terms were net 30. We weren't burning cash to fund growth. But we still had to model every cash outflow tied to the deal structure and make sure the business could service all of it without creating liquidity pressure.

The questions we were answering with that model: Can we support the seller note payments? Can we hit the retention comp timing? What does the management team's equity actually look like on exit, across a range of performance scenarios? What does the original seller's check look like at the second close?

You build the illustration to align stakeholders. You build the model to make sure the deal doesn't break.

What This Deal Actually Shows

At face value, this is a deal where a buyer paid 3.3x cash consideration for a business doing $3M in profit, structured installment payments around a contract renewal, and used the remaining consideration to incentivize a management team that wasn't otherwise going to stick around.

What it actually shows is something more useful: how you design a transaction when the asset you're acquiring isn't the business on paper — it's the people running it.

The owner had built a profitable business by surrounding himself with excellent operators and then stepping away. The problem for us as buyers was that those operators had no formal reason to stay. No equity, no long-term contracts, no structural alignment with the outcome of any transaction. The business was printing cash, but the future of that cash was entirely dependent on people whose future plans we couldn't control.

We couldn't just negotiate with the seller. We had to sell the deal to the team. We had to make the CEO a partner in structuring the consideration for his own people. We had to design an equity instrument that gave them a real stake in not just our hold period, but the next buyer's hold period too.

Deal design as a craft means understanding that the spreadsheet is only part of the answer. The rest of it is understanding the motivations of every constituency at the table, including the ones who technically aren't at the table, and building a structure that makes the deal work for all of them.

Listen to the Full Conversation

Peter Baldwin and I walk through the actual visual illustration in the video version of this episode. Download the file from the description if you're listening on audio and want to follow along with the numbers.

This is the kind of deal breakdown we do regularly inside our Agency M&A community. If you want to see more of how we think about deal design: not in the abstract, but against real numbers and real constraints, you can find everything in the description.